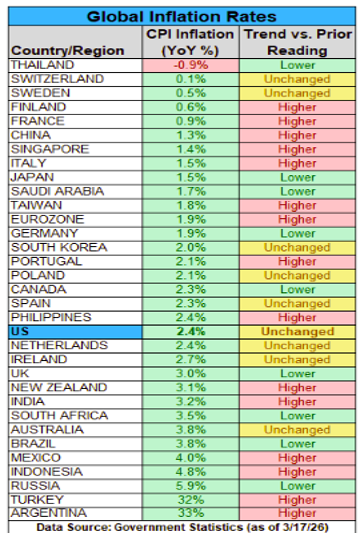

Central banks dominated the macro narrative this week, with major institutions maintaining rates while signaling a more cautious outlook amid rising inflation risks. In the US, housing indicators showed tentative improvement, but higher producer prices raised concerns about renewed inflation pressures. The Euro area saw weaker export performance alongside easing cost pressures, while China’s activity data pointed to modest improvement driven by industrial output and infrastructure investment, despite ongoing weakness in domestic demand.

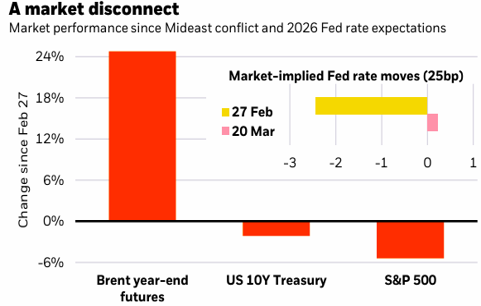

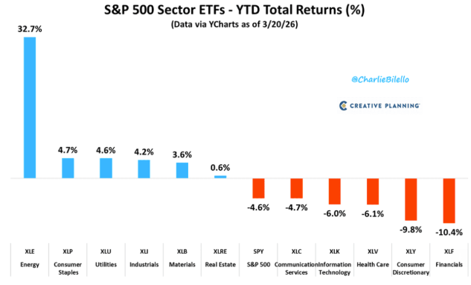

Markets reacted negatively as geopolitical tensions intensified, particularly in the Middle East. Equity markets declined across developed regions, with technology stocks and small caps under pressure, while emerging markets showed relative resilience. Bond markets benefited from lower yields, supporting investment-grade credit, and commodities were driven higher by energy supply concerns and safe-haven demand. The US dollar strengthened, while cryptocurrencies continued to weaken.

Download the full report below for detailed analysis, market data, and our assessment of the implications for global investors.